Page: 1

/ 14

Total 115 questions

AGA Examination 2: Governmental Accounting, Financial Reporting and Budgeting GAFRB Exam Questions

Question 1

The summary of significant accounting policies in the notes to the financial statements includes all of the following information EXCEPT

Answer : C

Question 2

A municipality would establish an internal service fund to capture the activities of a data processing center, in order to account for

Answer : D

Question 3

A private bank provides a student loan that the government has insured against default. This is an example of

Answer : B

Question 4

The roles of GASB and FASAB are to

Answer : C

Question 5

Which of the following fund types would be used to collect water utility user fees?

Answer : D

Question 6

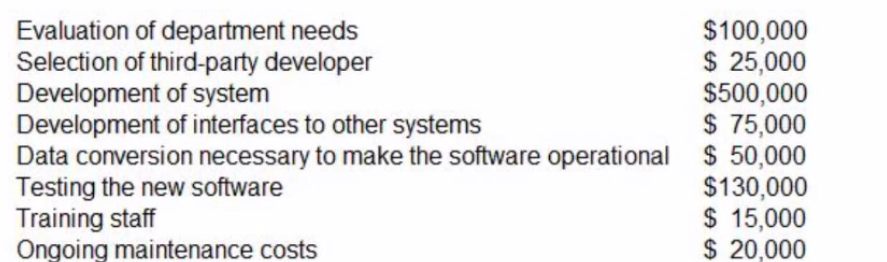

A state department has been developing a new computer system for managing federal grants. The project has the following costs:

What amount should be recorded as the value of the intangible asset?

Answer : C

Question 7

What is the annual projected sales tax revenue if in nine months the revenue earned is $26.5 million, and no other factors are known?

Answer : B