Page: 1

/ 14

Total 163 questions

AICPA CPA Financial Accounting and Reporting CPA-Financial CPA Exam Questions

Question 1

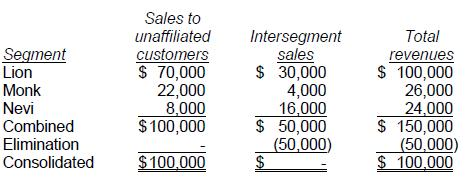

Terra Co.'s total revenues from its three operating segments were as follows:

Which operating segment(s) is (are) deemed to be reportable segments?

Answer : D

Choice 'd' is correct. A reportable operating segment is one having 10% of all revenue, including revenue from unaffiliated sales and from intersegment sales:

Lion's revenue percentage is 66.7% [$100,000/150,000].

Monk's revenue percentage is 17.3% [$26,000/150,000].

Nevi's revenue percentage is 16% [$24,000/150,000].

Thus, all three segments meet the 10% of total revenues test and are reportable as operating segments. SFAS 14 para. 10 and 15 as amended by SFAS 131

Choice 'a' is incorrect. All segments with revenue percentages exceeding 10% of total revenues are reportable operating segments.

Choice 'b' is incorrect. Lion is not the only segment with revenue percentages exceeding 10% of total revenues.

Choice 'c' is incorrect. Nevi has a revenue percentage exceeding 10% of total revenues.

Question 2

During 1990, Fuqua Steel Co. had the following unusual financial events occur:

* Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain. Fuqua has frequently retired bonds early when interest rates declined significantly.

* A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth similar loss sustained in a 5-year period at that location.

* A component of Fuqua's operations, steel transportation, was sold at a net loss of $350,000.

This was Fuqua's first divestiture of one of its operating segments.

Before income taxes, what amount of gain (loss) should be reported separately as a component of income from continuing operations in 1990?

Answer : B

Choice 'b' is correct. $5,000.

The steel forming segment's hurricane damage (4th in 5 years) of $255,000 is only 'unusual in nature' and does not occur infrequently, therefore, it is not an 'extraordinary item,' and should be reported separately as a component of 'income from continuing operations.'

The retirement of debt, although unusual, is not infrequent for the company; therefore, the gain does not qualify for classification as an extraordinary item per APBO No. 30 (and SFAS No. 145).

Question 3

On December 2, 20X1, Flint Corp.'s board of directors voted to discontinue operations of its frozen food division and to sell the division's assets on the open market as soon as possible. The division reported net operating losses of $20,000 in December and $30,000 in January. On February 26, 20X2, sale of the division's assets resulted in a gain of $90,000. Assuming that the frozen foods division qualifies as a component of the business and ignoring income taxes, what amount of gain/loss from discontinued operations should Flint recognize in its income statement for 20X2?

Answer : C

Choice 'c' is correct. The $60,000 gain from discontinued operations would be reported in Flint's 20X2 income statement. The operating loss for January would offset the gain from disposal in February, and the net amount would be reported as a gain (in this case) from discontinued operations.

The operating losses for December would have been reported in Flint's 20X1 income statement.

Choice 'a' is incorrect per the above. It would be correct if all of the gains and losses were included in 20X1 instead of 20X2. However, gains and losses from discontinued operations are included in the year they occur.

Choice 'b' is incorrect. It includes the operating loss for December, 20X1 in with the 20X2 amounts.

Choice 'd' is incorrect. It ignores the January operating loss. Operating losses are included in gain/loss from discontinued operations, along with impairment losses and gains/losses on disposal.

Question 4

On December 31, 20X2, the Board of Directors of Maxy Manufacturing, Inc. committed to a plan to discontinue the operations of its Alpha division. Maxy estimated that Alpha's 20X3 operating loss would be $500,000 and that the fair value of Alpha's facilities was $300,000 less than their carrying amounts.

Alpha's 20X2 operating loss was $1,400,000, and the division was actually sold for $400,000 less than its carrying amount in 20X3. Maxy's effective tax rate is 30%.

In its 20X2 income statement, what amount should Maxy report as loss from discontinued operations?

Answer : B

Choice 'b' is correct. Since the fair value of Alpha's facilities was $300,000 less than its carrying value, there has been an impairment loss, and that loss should be recognized in 20X2. That $300,000 impairment loss plus the $1,400,000 20X2 operating loss would be recognized in 20X2 net of tax. The total loss would be $1,700,000 70% (100% - 30%) or $1,190,000.

Choice 'a' is incorrect. It includes the 20X2 operating loss of $1,400,000 but not the $300,000 impairment loss but does report the 20X2 operating loss net of tax.

Choice 'c' is incorrect. It includes the 20X2 operating loss of $1,400,000, but not the $300,000 impairment loss, and reports the 20X2 operating loss gross of tax and not net of tax.

Choice 'd' is incorrect. It reports the 20X2 loss from discontinued operations gross of tax and not net of tax.

Question 5

According to the FASB conceptual framework, an entity's revenue may result from:

Answer : D

Rule: Revenues are inflows or other enhancements of assets and/or settlements (decreases) in liabilities resulting from the entity's ongoing major operations, not from 'incidental' operations.

Choice 'd' is correct. An entity's revenue may result from a decrease in a liability from primary operations.

Question 6

A transaction that is unusual, but not infrequent, should be reported separately as a(an):

Answer : D

Choice 'd' is correct. A transaction that is unusual, but not 'infrequent' should be reported separately as a component of continuing operations, (gross) but not net of applicable income taxes.

Choices 'a' and 'b' are incorrect. An extraordinary item has to be both 'unusual' and 'infrequent.'

Choice 'c' is incorrect, per 'd' above.

Question 7

Which of the following types of entities are required to report on business segments?

Answer : A

Choice 'b' is correct. Only publicly-traded enterprises are required to report on business segments.

Choices 'a', 'c', and 'd' are incorrect, per the Explanation: above.