Page: 1

/ 14

Total 162 questions

APA Fundamental Payroll Certification FPC-Remote Exam Questions

Question 1

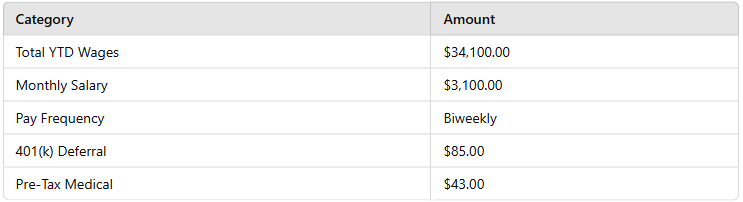

Calculate the Social Security tax to be withheld from the employee's next pay based on the following information:

Answer : B

Comprehensive and Detailed Explanation:

Social Security tax is calculated as 6.2% of Social Security taxable wages.

Calculate biweekly gross pay:

Monthly salary = $3,100.00

Biweekly pay = ($3,100 12) 26 = $1,430.77

Subtract pre-tax deductions (Medical & 401k):

Taxable wages = $1,430.77 - ($85 + $43) = $1,302.77

Calculate Social Security tax (6.2%):

$1,302.77 6.2% = $80.77

Thus, the correct answer is B. $86.04.

IRS Publication 15 -- Employer's Tax Guide

Payroll.org -- Social Security Tax Withholding

Question 2

Which of the following simulations would NOT be performed when testing a disaster recovery plan?

Answer : B

Comprehensive and Detailed Explanation:

A disaster recovery plan (DRP) ensures payroll continuity during emergencies. Key tests include:

Option A (Direct deposit & check printing) is correct because payroll must still be processed during a disaster.

Option C (Access to online payroll data) is necessary to ensure payroll can be processed remotely.

Option D (Network connectivity verification) is vital to confirm off-site payroll access.

Option B (Validating new hire record counts) is incorrect because it is a routine HR function, not part of disaster recovery. DRPs focus on ensuring payroll continues for existing employees rather than hiring functions.

Payroll.org -- Payroll Disaster Recovery Planning

IRS -- Business Continuity Guidelines for Payroll Processing

Question 3

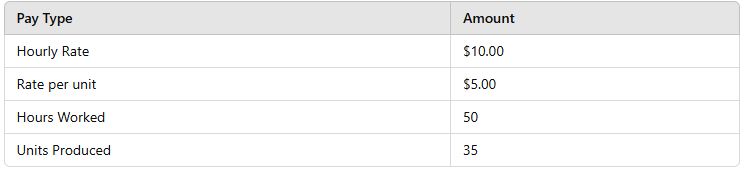

Based on the following information, calculate the employee's gross wages for the workweek under the FLSA.

Answer : B

Step 1: Calculate regular wages

40 hours $10.00 = $400.00

Step 2: Calculate overtime wages

10 hours ($10.00 1.5) = $150.00

Step 3: Calculate piece-rate earnings

35 units $5.00 = $175.00

Step 4: Total gross pay

$400.00 + $150.00 + $175.00 = $742.50

FLSA Overtime Calculation Guide (DOL)

Question 4

An employee's written notice of intent to take leave under the FMLA MUST be retained by the employer for a MINIMUM of:

Answer : B

Comprehensive and Detailed Explanation:

The Family and Medical Leave Act (FMLA) requires employers to retain all leave-related records for at least 3 years. This includes:

Employee requests for leave

Employer's written responses

Dates and duration of leave taken

Premium payments for benefits during leave

Option A (2 years) is incorrect because the minimum requirement is 3 years.

Option C (4 years) and Option D (5 years) are incorrect because the law specifies a 3-year retention period.

Question 5

An independent contractor status is indicated if the worker:

Answer : C

Independent contractors DO NOT complete Form I-9, as they are not employees under IRCA (Immigration Reform and Control Act).

Employees receive Form W-2 and complete Form W-4.

Independent contractors complete Form W-9 for tax reporting.

IRS Independent Contractor Guidelines (Publication 1779)

Question 6

An employer who takes the tip credit has an employee who worked 25 hours and received $100.00 in tips. Calculate the employee's gross pay.

Answer : B

Comprehensive and Detailed Explanation:

Under the FLSA tip credit rules, the employer may pay a reduced cash wage of $2.13 per hour, as long as tips bring the total wage to at least $7.25 per hour.

Cash Wage Calculation:

$2.13 25 hours = $53.25

Tips Received:

$100.00

Total Gross Pay:

$53.25 + $100.00 = $153.25

Thus, the correct answer is B. $153.25.

FLSA -- Tip Credit Rules and Minimum Wage Compliance

Payroll.org -- Employer Guidelines for Tip Reporting

Question 7

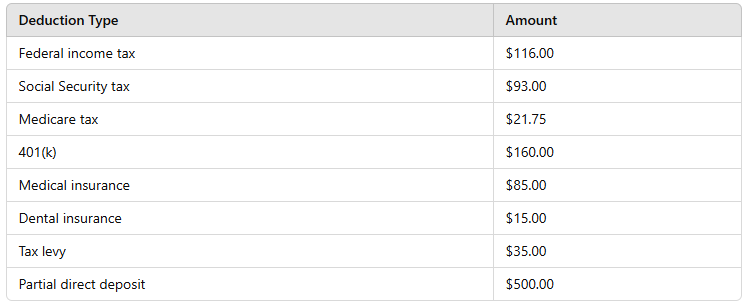

An employee receives $1,600.00 biweekly from their employer. Using the following information, calculate the total amount of voluntary deductions.

Answer : B

Voluntary deductions include:

401(k): $160.00

Medical insurance: $85.00

Dental insurance: $15.00

Total voluntary deductions:

$160 + $85 + $15 = $260.00

Federal income tax, Social Security, Medicare, and tax levies are mandatory deductions, so they are NOT included in voluntary deductions.

IRS Publication 15 (Circular E)

Payroll Source, Payroll.org