Page: 1

/ 14

Total 715 questions

CFA Institute CFA Level II Chartered Financial Analyst CFA-Level-II Exam Questions

Question 1

Charles Mabry manages a portfolio of equity investments heavily concentrated in the biotech industry. He just returned from an annual meeting among leading biotech analysts in San Francisco. Mabry and other industry experts agree that the latest industry volatility is a result of questionable product safety testing methodologies. While no firms in the industry have escaped the public attention brought on by the questionable safety testing, one company in particular is expected to receive further attention---Biological Instruments Corporation (BIC), one of several long biotech positions in Mabry's portfolio. Several regulatory agencies as well as public interest groups have heavily criticized the rigor of BIC's product safety testing.

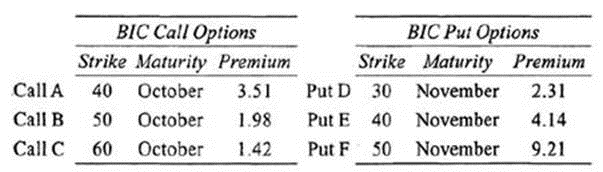

In an effort to manage the risk associated with BIC, Mabry has decided to allocate a portion of his portfolio to options on BIC's common stock. After surveying the derivatives market, Mabry has identified the following European options on BIC common stock:

Mabry wants to hedge the large BIC equity position in his portfolio, which closed yesterday (June 1) at $42 per share. Since Mabry is relatively inexperienced with utilizing derivatives in his portfolios, Mabry enlists the help of an analyst from another firm, James Grimell.

Mabry and Grimell arrange a meeting in Boston where Mabry discusses his expectations regarding the future returns of BIC's equity. Mabry expects BIC equity to make a recovery from the intense market scrutiny but wants to provide his portfolio with a hedge in case BIC has a negative surprise. Grimell makes the following suggestion:

"If you want to avoid selling the BIC position and are willing to earn only the risk-free rate of return, you should sell calls and buy puts on BIC stock with the same market premium. Alternatively, you could buy put options to manage the risk of your portfolio. I recommend waiting until the vega on the options rises, making them less attractive and cheaper to purchase."

Assuming that on October 15, the closing price of BIC common stock is $40 per share, how would the delta of Put F have changed from June 1?

Answer : A

As the option moves further into the money and as the expiration date approaches, the delta of a put option moves closer to -1. (Study Session 17, LOS 60.e)

Question 2

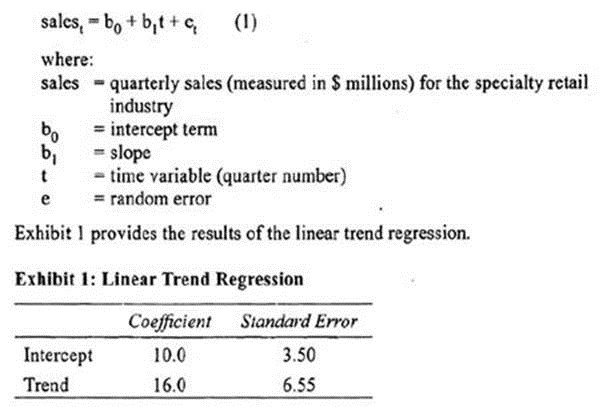

William Shears, CFA, has been assigned the task of predicting sales for the specialty retail industry. Shears finds that sales have been increasing at a fairly constant rate over time and decides to estimate the linear trend in sales for the industry using quarterly data over the past 15 years, starting with Quarter 1 of 1994 and ending with Quarter 4 of 2008. On January 1, 2009, Shears estimates the following model:

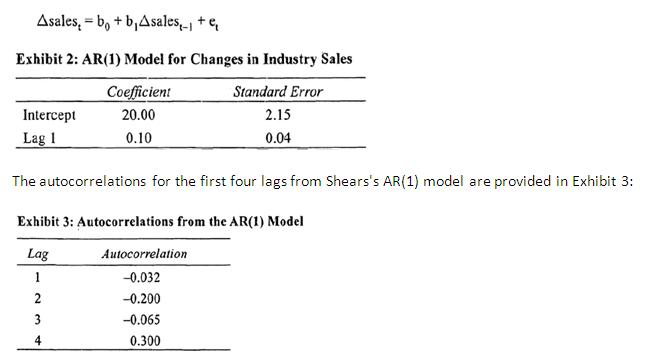

Shears also estimates an autoregressive model of order one, AR(1), using the changes in quarterly sales data for the industry from the first quarter of 1994 through the fourth quarter of 2008. He obtains the following results for his AR(1) model:

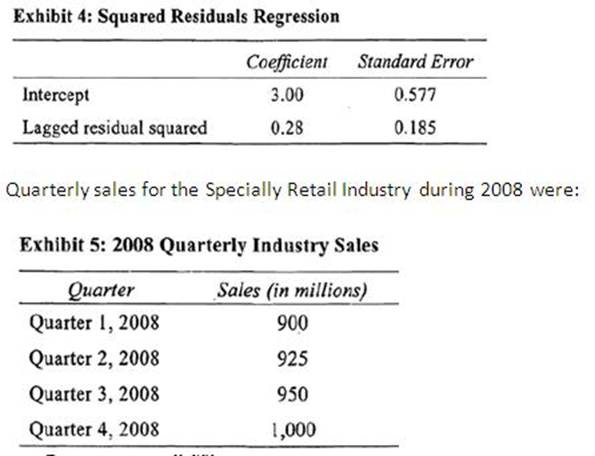

Shears also derives a regression using the residuals from the AR(1) model. He regresses the squared residuals (or estimated errors) against the lagged squared residuals. The results of this regression are reported in Exhibit 4.

Quarterly sales for the Specially Retail Industry during 2008 were:

Shears's supervisor, Sam Kite, expresses concern that equation (1) might be misspecified. Specifically, Kite refers to the finding that "sales have been increasing at a fairly constant rate over time.

Using the results for the linear trend equation in Exhibit 1, the specialty retail industry sales forecast for Quarter 1 of 2009 is closest to:

Answer : C

Quarter 1 of 2009 is the 61st quarter (starting with Quarter 1 of 1994): sales = 10 + 16(61) = $986 million. (Study Session 3, LOS 13.a)

Question 3

Carol Blackwell, CFA, has been hired to manage trust assets for Blanchard Investments. Blanchard's trust manager, Thaddeus Baldwin, CFA, has worked in the securities business for more than 50 years. On Blackwell's first day at the office, Baldwin gives her several instructions.

Instruction 1: Limit risk by avoiding stock options.

Instruction 2: Above all, ensure that our clients' capital is kept safe.

Instruction 3: We take pride in our low cost structure, so avoid unnecessary transactions.

Instruction 4: Remember that every investment must have the quality to stand on its own.

Baldwin realizes that many of the firm's practices and policies would benefit from a compliance check. Because Blackwell recently received her CFA charter, Baldwin tells her she is the "perfect person to work with the compliance officer to update the policy on proxy voting and the procedures to comply with Standard VI(B) Priority of Transactions." Baldwin also wants Blackwell to evaluate whether the firm wants to, or can, claim compliance with the soft dollar standards. Baldwin hands Blackwell a handwritten outline he created, which includes the following statements:

Statement 1: CFA Institute's soft-dollar rules are not mandatory. In any case, ' client brokerage can be used to pay for a portion of mixed-use research.

Statement 2: Investment firms can use client brokerage to purchase research that does not immediately benefit the client. Commissions generated by outside trades are considered soft dollars, but commissions from internal trading desks are not.

During a local society luncheon, Blackwell is seated next to CFA candidate Lucas Walters, who has been assigned the task of creating a compliance manual for Borchard & Sons, a small brokerage firm. Walters asks for her advice.

When Walters returns to work, he is apprised of the following situation: Borchard & Sons purchased 25,000 shares of CBX Corp. for equity manager Quintux Quantitative just minutes before the money manager called back and said it meant to buy 25,000 shares of CDX Corp. Borchard then purchased CDX shares for Quintux, but not before shares of CBX Corp. declined by 1.5%. The broker is holding the CBX shares in its own inventory.

Borchard proposes three methods for dealing with the trading error.

Method 1: Quintux directs additional trades to Borchard worth a dollar value equal to the amount of the trading loss.

Method 2: Borchard receives investment research from Quintux in exchange for Borchard covering the costs of the trading error.

Method 3: Borchard transfers the ordered CBX shares in its inventory to Quintux, which allocates them to all of its clients on a pro-rata basis.

Are Thaddeus Baldwin's statements on the soft dollar standards correct?

Answer : B

Commissions from both internal and external brokerage operations are considered soft dollars, so Statement 2 is false. Statement 1 is true. CFA Institute Soft Dollar Standards are voluntary, though firms that wish to claim compliance with the Standards must follow them completely. Client brokerage can be used to pay for mixed-use research with the caveat that the research must be reasonable, justifiable, and documcntable, and that the client brokerage is only used to pay for the portion of the research that will be used in the investment decision-making process. While research paid for by client brokerage should directly benefit the client, it does not have to do so immediately. (Study Session 1, LOS 3-b)

Question 4

Mary Andrews and Drew McClure are economists for Gasden Econometrics. Gasden provides economic consulting and forecasting services for governments, corporations and small businesses. Andrews and McClure are currently consulting for the developing country of Wakulla, which is considering imposing new regulations on its businesses.

Due to increases in industrial production in the country, the demand for electricity has increased. Unfortunately the cost of electricity has increased as well, and the Wakullian government is considering regulating the electrical utility industry by limiting the amount producers can charge. The price limits would be established so that the utilities can set their own prices as long as they do not earn a return on invested capital that is higher than the average Wakullian business.

The Wakullian government has also proposed stiffer environmental regulations on its firms because the level of air quality has declined in its largest cities. Andrews advises that this regulation is likely to increase production costs that will burden smaller businesses more than larger businesses, and thus can adversely affect competition within an industry. The higher production cost from the environmental regulation will ultimately be borne by consumers, she asserts.

One of the concerns of the Wakullian government is that previous regulation of the economy has been ineffective. For example, when the automobile industry was required to increase the fuel efficiency of passenger vehicles, they increased the weight of some vehicles so more could be classified as trucks, instead of passenger vehicles. The trucks were not subject to the regulation and as a result, fuel efficiency actually declined in the country due to the heavier weight of trucks. McClure comments that the regulation should have been written so that the regulation would be more effective.

McClure gives another example of an ineffective regulation from the automobile industry. When airbags were required in automobiles, consumers started wearing their seat belt less often and driving at higher speeds because the airbags gave them a feeling of greater safety. Consequently, driving fatalities and injuries did not decline as much as expected.

Some regulation, Andrews states, is limited in effectiveness when the regulators are chosen from the industry that is regulated. For example, Andrews states that, due to the level of scientific knowledge needed, many regulatory bodies for the pharmaceutical industry are dominated by former drug company executives and scientists. She states that, according to the share-the-gains, share-the-pains theory, regulatory decisions tend to favor the drug industry because of the close relationship between the industry and the regulator.

McClure adds that another example of regulatory ineffectiveness is when telephone companies go before their regulatory bodies to ask for rate increases. He states ihat according to the capture hypothesis, telephone companies will have greater economic resources and more at stake than individual consumers. As a result, the regulatory decisions tend to favor the telephone industry.

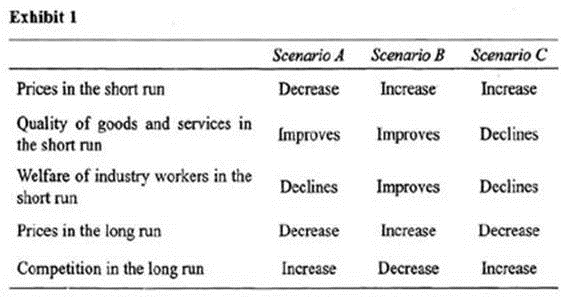

The Wakullian government is considering some of the country's industries. To illustrate the potential costs and benefits of deregulation to the Wakullian government, Andrews and McClure compose a matrix of the potential consequences of deregulation. In the matrix, three scenarios of possible economic consequences are presented in Exhibit 1.

Which of the following terms best describes the response of consumers to the auto safety regulation?

Answer : A

The response of consumers to the auto safety regulation is best described as a feedback effect. A feedback erfect is an example of a creative response, where the intent o( the original regulation is undermined. (Study Session 4, LOS 15-b)

Question 5

Sara Robinson and Marvin Gardner are considering an opportunity to start their own money management firm. Their conversation leads them to a discussion on establishing a portfolio management process and investment policy statements. Robinson makes the following statements:

Statement 1;

Our only real objective as portfolio managers is to maximize the returns to our clients.

Statement 2:

If we are managing only a fraction of a client's total wealth, it is the client's responsibility, not ours, to determine how their investments are allocated among asset classes.

Statement 3: When developing a client's strategic asset allocation, portfolio managers have to consider capital market expectations. In response, Gardner makes the following statements:

Statement 4: While return maximization is important for a given level of risk, we also need to consider the client's tolerance for risk.

Statement 5: We'll let our clients worry about the tax implications of their investments; our time is better spent on finding undervalued assets.

Statement 6: Since we expect our investor's objectives to be constantly changing, we will need to evaluate their investment policy statements on an annual basis at a minimum.

Robinson wants to focus on younger clientele with the expectation that the new firm will be able to retain the clients for a long time and create long-term profitable relationships. While Gardner felt it was important to develop long-term relationships, he wants to go after older, high-net-worth clients.

Are Statements 2 and 3 correct when considering asset allocation?

Answer : C

Strategic asset allocation requires investment managers to consider all sources of income and risk. It also requires an analysis of capital market conditions and specific risk and return characteristics of individual assets. Therefore, Statement 2 is incorrect, and Statement 3 is correct. (Study Session 18, LOS 68.e)

Question 6

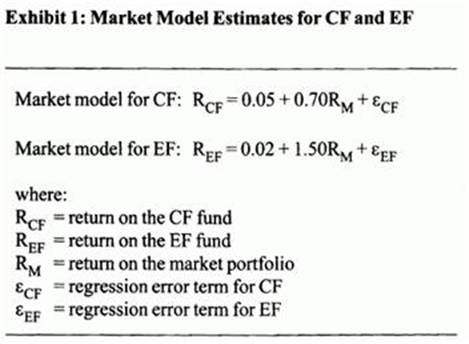

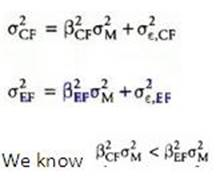

Factor Analytics Capital Management makes portfolio recommendations using various factor models. Mauricio Rodriguez, a Factor Analytics research analyst, is examining the prospects of two portfolios, the FACM Century Fund (CF) and the FACM Esquire Fund (EF).

The variance of returns are identical for the two funds. The estimates in Exhibit 1 were derived for CF and EF using monthly data for the past five years.

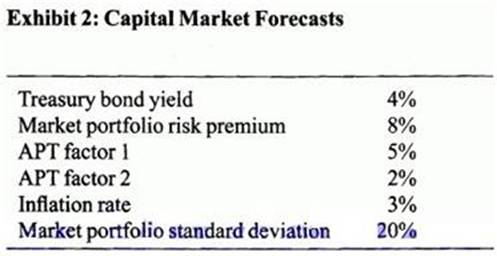

Supervisor Barbara Woodson asks Rodriguez to use the Capita! Asset Pricing Model (CAPM) and a multifactor model (APT) to make a decision to continue or discontinue the EF fund. The two factors in the multifactor model are not identified. To help with the decision, Woodson provides Rodriguez with the capital market forecasts in Exhibit 2.

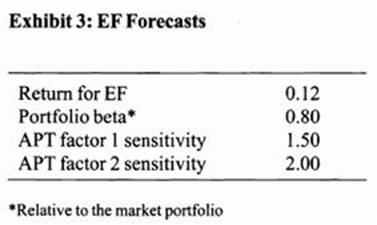

After examining the prospects for the EF portfolio, Rodriguez derives the forecasts in Exhibit 3.

Rodriguez also develops a 2-factor macroeconomic factor model for the EF portfolio. The two factors used in the model are the surprise in GDP growth and the surprise in Investor Sentiment. The equation for the macro factor model is:

During an investment committee meeting, Woodson makes the following statements related to the 2-factor macroeconomic factor model.

Statement 1: An investment combination in CF and EF that provides a GDP growth factor beta equal to one and an Investor Sentiment factor beta equal to zero will have lower active factor risk than a tracking portfolio consisting of CF and EF.

Statement 2: When markets are in equilibrium, no combination of CF and EF will produce an arbitrage opportunity

In their final meeting, Rodriguez informs Woodson that the CF portfolio consistently outperformed its benchmark over the past five years. Rodriguez makes the following comments to Woodson: "The consistency with which CF outperformed its benchmark is amazing. The difference between the CF monthly return and its benchmark return was nearly always positive and varied little over time."

Using the market model estimates for CF and EF, which fund has higher:

Systematic risk? Unsystematic risk?

Answer : C

The slope of the market model is the beta. Systematic risk is high for high beta funds. From Exhibit 1, the market beta is lower for CF (0.70) versus EF (1.50). Unsystematic risk is measured by the variance of the market model error (e). The information provided in the vignette states that the variances are identical for CF and EF. We can determine which fund has larger unsystematic risk by using the market model formula for the variance:

because the bera is smaller for CF versus EF. The vignette states that the variances for CF and EF are identical. Therefore, if the total variances are identical, and if the first component is smaller for CF versus EF, then the second component (unsystematic risk) must be larger for CF versus EF. (Study Session 18, LOS 64.f,g)

Question 7

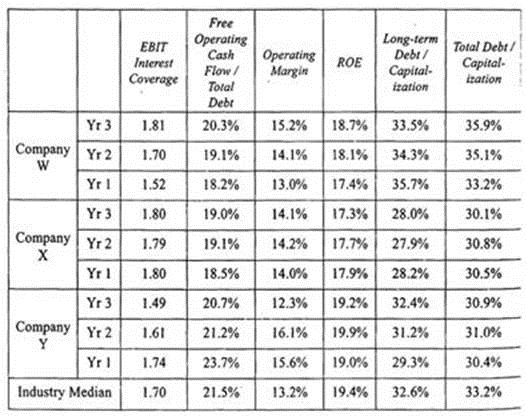

Michael Thomas, CFA, is a fixed-income portfolio manager for TFC Investments. As part of his portfolio strategy for the Prosperity Fund, Thomas searches for companies that he expects to be upgraded or downgraded. Those potential upgrades he finds are added to the portfolio or if already in the portfolio are increased in proportion to other holdings before the upgrade takes place. Potential downgrades are sold from the portfolio before the downgrade takes place. Thomas is evaluating his portfolio's current holdings which include several bonds issued by companies in the oil and gas exploration and refining industries. Year-end rating updates are expected to occur in a few days and Thomas is preparing to adjust his portfolio based on expected changes in credit ratings. He has assembled the following annual data on four of the oil and gas stocks in the portfolio:

Exhibit: 1

Thomas has been discussing his fixed-income strategies with a fellow portfolio manager, Shawna Reese. Reese has indicated that while his initial approach is good, the overall credit analysis strategy could be improved and has made the following suggestions to Thomas for both the Prosperity Fund and other fixed-income funds he manages:

* The current methodology does not consider special issues related to high-yield debt which makes up approximately 5% of the Prosperity Fund. Because most high-yield issuers have such a heavy dependence on short-term debt financing, analysis of the firm's debt structure will be extremely important to determine the priority of claims on the firm's assets as well as what source(s) of funds will be used to repay the principal. In addition, the corporate structure of high-yield issuers must be examined to determine the issuer's access to cash flows generated by its subsidiaries. A simple analysis of the parent's financial ratios will not reveal complicated corporate structures and indebtedness of subsidiaries that may restrict the issuer's ability to obtain the cash flows necessary to service its debt.

* The current methodology as applied to the Municipal Opportunities Fund does not include the necessary specialized analysis for municipal securities. Among other items, tax-backed munis must be scrutinized as to the issuer's ability to maintain balanced budgets as well as to ensure that the issue has first priority of claims to revenue from public works projects. Revenue-backed munis require an assessment of the sufficiency of rate covenants to cover expenses and debt servicing of the underlying project as well as the ability for other government entities to access the revenues generated by the enterprise before they are passed on to revenue bondholders.

As part of his portfolio analysis, Thomas also examines yield volatility. Thomas makes the following statements:

Statement 1: Implied yield volatility estimates are based on the assumptions that the option pricing model is correct and that volatility is constant.

Statement 2: Yield volatility has been observed to follow patterns over time that can be modeled and used to forecast future volatility.

He concludes his analysis by comparing the swap rate curve to a government bond yield curve as a benchmark.

Which of the following statements regarding the choice between government bond yield curves and swap rate curves as benchmark yields is most likely correct?

Answer : A

Market participants typically prefer to use the swap rate curve as a benchmark for the following reasons;

* The availability of swaps and the equilibrium pricing arc only driven by the interaction of supply and demand. It is not affected by technical market factors that can affect government bond yields.

* Swap curves across countries arc also more comparable than sovereign bond yield curves because they reflect similar levels of credit risk, while sovereign bond yield curves also reflect credit risk unique to each country's government bonds.

* The swap curve typically has yield quotes at 11 maturities between 2 and 30 years. The U .S . government bond yield curve typically only has on-che-run issues trading at four maturities between 2 and 30 years.

* . The swap market is not regulated by any government, which makes swap rates

across different countries more comparable.

(Study Session 14, LOS 53.d)