Page: 1

/ 14

Total 248 questions

CIMA F2 Advanced Financial Reporting CIMAPRA19-F02-1 Exam Questions

Question 1

What is the total comprehensive incomeattributable tothe non-controlling interestthat will be presented in GHI's consolidated statement of changes in equity for the year ended 31 December 20X4?

Answer : A

Question 2

ST granted 1,000 share appreciation rights (SARs) to its 100 employees on 1 December 20X7. To be eligible, employees must remain employed for 3 years from the grant date.In the year to 30 November 20X8, 10 staff left and a further 20 were expected to leave over the following two years. The fair value of each SAR was $12 at 1 December 20X7 and $15 at 30 November 20X8.

What is the accounting entry to record this transaction for the year to 30 November 20X8?

Answer : A

Question 3

LM and JK operatein the same countryand prepare their financial statements to30 June 20X6 in accordance with International Accounting Standards. On 27 June 20X6 both entities raised $1 million cashby issuing debt instruments with identical terms and conditions. Prior to this issue both entities were financed entirely by equity.

At 30 June 20X6 the gearing ratios,calculatedasDebt/Equity x 100%, wereas follows:

LM: 30%

JK: 65%

Which of the following independent options would explain the difference between LM and JK's year-end gearing?

Answer : A

Question 4

Which of the following statements about ST is true?

Answer : B

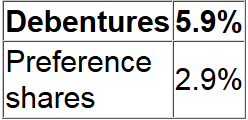

Question 5

UV has raised $100,000 through theissue of two irredeemable financial instruments:

* 6% debentures with a current market value of $101.50 per $100 nominal value; and

* 8% preference shares with a current share price of $2.20 each.

The corporateincometax rate is 20%

What is the post tax cost of debt foreach of theseinstruments?

Answer : A

Question 6

AB, a listed entity, prepared its financial statements to 31 December 20X7, in accordance with international accounting standards.

Which THREE of the following were disclosed as related parties of AB in its financial statements?

Answer : A, B, C

Question 7

Which THREE of the followingwould typically indicate a finance lease?

Answer : A, C, E