Page: 1

/ 14

Total 50 questions

Guidewire ClaimCenter Business Analyst Exam (Mammoth Proctored Version) ClaimCenter-Business-Analysts Exam Questions

Question 1

When creating a new Personal Auto claim, Succeed Insurance would like to identify when Rideshare is the primary use for a vehicle. A Business Analyst (BA) thinks that Primary Use already exists as a typekey on the Vehicle Details screen.

What are two ways the BA can confirm whether this field is configured in ClaimCenter and, if it is, which values are available in the typelist? (Choose two.)

Answer : A, D

To verify the configuration of a specific field and its available values (typelist) within a specific implementation (like Succeed Insurance), a Business Analyst must consult the sources that reflect the current, actual system configuration, not just the out-of-the-box documentation.

Option A (Data Dictionary): The Data Dictionary is the definitive, generated documentation of the running application's data model. It lists all Entities (such as Vehicle) and their Typekeys (such as PrimaryUse). By navigating to the Data Dictionary, a BA can confirm if the field exists in the database schema and view the specific Typelist values (e.g., 'Rideshare', 'Commuting', 'Pleasure') associated with it. This is a primary tool for BAs to understand the data structure.

Option D (Guidewire Studio): Guidewire Studio is the Integrated Development Environment (IDE) used to configure the application. It contains the 'Source of Truth' for all configuration files. A BA (or a developer assisting them) can open the Page Configuration (PCF) files to see the Vehicle Details screen definition or open the Typelist files (.tti/.ttx) directly to see exactly which values are defined and active.

Why other options are incorrect:

Option B (Application Guide): The Application Guide documents the Base (Out-of-the-Box) product features. It does not contain customer-specific customizations or extensions. If 'Primary Use' or 'Rideshare' were added or modified by Succeed Insurance, the Application Guide would not reflect this.

Option C (UI Inspection with CTRL+F): While logging into the application allows a user to see the dropdown on the screen, the shortcut CTRL + F is merely the browser's 'Find' function. It searches visible text on the page but does not provide configuration metadata, hidden values, or definitive proof of the underlying data model structure. The correct shortcut for inspecting widget properties in Guidewire is Alt + Shift + I (Location Info), but even that is less efficient for viewing a full typelist than the Data Dictionary or Studio.

Question 2

Succeed Insurance has plans to expand operations in Greeley, Colorado. Due to a history of hailstorm related damage in the area, the company plans to offer reimbursement for hail damage as an option.

Which two actions should the Business Analyst (BA) take to determine the requirements for the project? (Choose two.)

Answer : A, B

In the Guidewire delivery methodology, the 'Determine Requirements' phase (often part of Inception or Elaboration) focuses on understanding the business need and mapping it to the software capabilities.

Lead an Elaboration Workshop (A): The Elaboration Workshop is the primary forum where BAs engage with stakeholders (like the Greeley operations team) to discuss the specific needs for the new 'hail damage' product. This is where the raw requirements are gathered, discussed, and refined.

Recommend Base Product Features (B): A critical responsibility of the Guidewire BA is to maximize product value by reducing unnecessary customization. When determining requirements for 'reimbursement' and 'hail damage,' the BA should immediately demonstrate and recommend how ClaimCenter's out-of-the-box Coverage, Exposure, and Incident features can handle this scenario. This aligns the customer's expectations with the standard software capabilities, expediting the implementation.

Why not C or D? Authoring user stories (C) and defining typelists (D) are outputs or tasks that occur after the requirements have been determined and the solution approach (Standard vs. Custom) has been agreed upon.

Question 3

An Adjuster at Succeed Insurance creates a check with a partial payment of $1,200 for medical expenses payable to a claimant who was injured in a collision. The check has completed the following processing steps:

. The payment exceeded the Adjuster's authority limits, changing the status to Pending Approval.

. The Adjuster's supervisor reviewed and approved the payment, changing the status to Awaiting Submission.

. A batch process sent the check to the external check processing system, changing the status to Requested when ClaimCenter received an update from the external system.

The Adjuster received new information indicating that the check amount should be reduced to $950.

Which action should the Adjuster take?

Answer : D

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

In the lifecycle of a check within Guidewire ClaimCenter, the Requested status indicates that the payment instruction has been successfully handed off to the downstream check writing or electronic funds transfer system. Once a check reaches this status, it is considered a committed financial transaction and is locked from further editing.

Why Option A is incorrect: You cannot edit a check that is in 'Requested' status. The 'Edit' button will likely be disabled or the fields locked because the data has already left the system.

Why Option C is incorrect: A 'Stop' payment is typically reserved for scenarios where a physical check has been lost, stolen, or destroyed after it was printed and mailed. While a Stop Payment does prevent the check from being cashed, it is a specific banking process often involving fees.

Why Option D is Correct: To correct an administrative error (such as the wrong amount) for a check that has been processed but not yet negotiated (cashed), the standard procedure is to Void the check. Voiding the check in ClaimCenter performs two critical functions:

It reverses the financial T-accounts (reserves and payments) associated with the transaction, ensuring the claim financials are accurate.

It updates the status to 'Voided,' effectively cancelling the payment in the system.

After voiding the incorrect check ($1,200), the Adjuster must then create a new check for the correct amount ($950) to pay the claimant.

Question 4

Succeed Insurance requires that a new 'Driver under 18?' field be added to the vehicle incident screen for personal auto claims to indicate whether or not the driver of the vehicle was a minor when the loss occurred. The field will be set by calculating the driver's age using the date of loss and the driver's date of birth.

There are two validation requirements:

The field must be set if the 'Date of Birth' field for the driver is not null.

No payments can be made for collision exposures if the 'Date of Birth' field for the driver of the vehicle is null.

A Business Analyst (BA) documents the validation requirements in the validation tab of the User Story Card 'Adjudicate - Update Maintain Vehicle Incident for Personal Auto Claims' as shown in the exhibit.

What information in the two validation examples is either missing or incorrectly documented? (Choose two.)

Answer : C, D

The User Story Card exhibit contains several documentation errors when compared to standard Guidewire requirements gathering best practices and the specific scenario provided.

Missing Requirement Number and Logic Gap (Option C):

Traceability: In the second row of the exhibit (the payment validation rule), the 'Requirement Number' column is completely blank. Traceability back to the original requirements document is mandatory for all entries.

Logic Precision: The requirement explicitly states that the rule applies to 'personal auto claims'. However, the logic documented in the 'Rules' column (If Exposure Type = VehicleDamage Then Block...) does not check the Policy Type. It relies solely on the Exposure Type, which could exist on Commercial Auto policies as well. To accurately reflect the business requirement, the condition If PolicyType = Personal Auto must be added (similar to how it was done in the first row).

Missing DV/LV Context for Validation (Option D):

UI Anchoring: The second requirement is a validation rule that triggers an error ('Driver's Date of Birth is required...'). For the system to highlight the specific field on the screen (the 'Driver Date of Birth' widget) when the error occurs, the rule must be associated with the specific Detail View (DV) or List View (LV) where that field resides (e.g., VehicleIncidentDV). The exhibit lists 'Not Applicable' in the 'Name of DV or LV' column. This is incorrect because providing the DV name ensures the error message is displayed contextually next to the field rather than as a generic page-level error, improving the user experience.

Why other options are incorrect:

Option A: The LOB column is used for filtering, reporting, and release management. Even if the rule logic checks the policy type, the LOB column is required metadata and should not be removed.

Option B: While the first requirement (the calculation) lacks a DV name (which it should have), it is a Business Rule (assignment), not a validation. Therefore, it does not generate an error or warning message for the user, so the second part of Option B is incorrect.

Option E: The 'Rules' column is exactly where the calculation logic (Date of Loss - Date of Birth) belongs. The developer needs this information to implement the automation.

Question 5

An Adjuster at Succeed Insurance increases the reserve on a claim's exposure from $1,000 to $1,500 to account for inflation in repair costs. A week later, a Supervisor reviews the claim and wants to know specifically who made this change, the exact date and time it was made, and what the previous value was.

The Supervisor needs a chronological audit trail of changes to the claim file without navigating through complex financial ledgers.

Which screen in the ClaimCenter user interface should the Supervisor access to find this information?

Answer : B

In Guidewire ClaimCenter, the History screen serves as the automated audit trail for the claim file. It is designed to capture and display a chronological list of significant events and user actions that have occurred throughout the claim's lifecycle.

Audit Trail Functionality: The History screen automatically records specific types of events, including:

Field Changes: When critical fields (like Reserve Amounts) are modified, the system logs the 'Old Value' and the 'New Value.'

Assignment Changes: Tracks when the claim was transferred from one user to another.

Rule Execution: Logs when specific business rules (like 'Exception Flagged') are triggered.

Data Points: For each entry, the History screen displays the User who performed the action, the Timestamp of the event, and a Description of the change.

Why other options are incorrect:

Financials > Transactions (A): While this screen shows the financial T-account entries (debits/credits) for the reserve increase, its primary purpose is accounting analysis. It is less efficient for a supervisor looking for a simple 'Who/When/What' audit trail compared to the History screen.

Notes (C): Notes are typically used for qualitative narratives and manual entry. While a system note can be generated for a reserve change, the History screen is the dedicated, non-editable system of record for tracking field changes.

Loss Details > Status (D): This screen shows the current state of the claim (e.g., Open, Closed, Litigation Status) but does not provide a historical log of previous values or the specific user actions that led to the current state.

Question 6

During claim intake and adjudication, Adjusters capture contact information for the insured and all claimants. To improve customer service and reduce the time required to reach these contacts to gather additional claim information, Succeed Insurance will capture the preferred contact method for all person contacts. The new field will be added to the contact details screen of the user interface (UI) as a drop-down list displaying all valid contact methods including email, mail, and phone.

Which version correctly lists the preferred contact methods in the Typelists tab of the Parties Involved User Story Card?

Answer : B

To correctly document a Typelist in a User Story Card, the Business Analyst must understand both the data structure (Codes vs. Names) and the configuration state (New vs. Modified).

Code Validity: In Guidewire, a Typecode (the value stored in the database) must be a unique identifier for each option in the list.

Option B correctly lists distinct codes: email, mail, and phone.

Options A and C are incorrect because they list the Typelist Name (PreferredContactMethod) as the Code for every single row. You cannot have multiple entries with the same primary key (Code) in one list.

Configuration State (New vs. Modified): The PreferredContactMethod typelist is a standard Base Product feature in Guidewire ClaimCenter. It already exists out-of-the-box.

Option B correctly identifies the Status as 'Modified'. When you add values to or configure an existing base typelist, you document it as 'Modified'.

Option D is incorrect because it lists the Status as 'New'. This would imply creating a brand new custom typelist (e.g., MyCustomList_Ext), which is not necessary for standard contact methods.

Therefore, Option B is the only version that has valid, unique codes and the correct configuration status.

Question 7

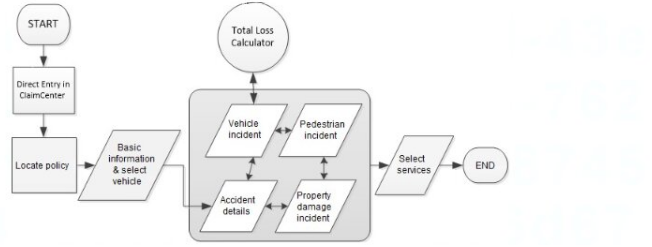

Whenever the Total Loss Calculator determines that a vehicle is a total loss, Succeed Insurance wants to create a custom history event with the exposure name and total loss score.

Which step in the claim setup process flow must be completed before the history event can be created?

Answer : C

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

In Guidewire ClaimCenter workflow analysis and configuration, defining the correct sequence of operations is critically dependent on Data Availability and Data Dependency.

The specific requirement here dictates that the custom history event must capture the Total Loss Score. In the context of the ClaimCenter object model and process flow, the Total Loss Score is an output value generated specifically by the Total Loss Calculator engine. Before this calculator runs, the score attribute is effectively null or non-existent.

Therefore, to satisfy the business requirement, the step that writes the history event must be placed after the step that generates the data it needs to record.

Process Logic: If the Business Analyst were to place the history event creation step before the Total Loss Calculator (Option B) or before the Vehicle Incident (Option D), the system would attempt to write a record containing a score that has not yet been calculated. This would result in either a system error or a history event with a blank/zero value, failing to meet the business requirement.

Dependency Chain: The workflow dependency is: Vehicle Data Entry -> Total Loss Calculation -> Score Generation -> History Event Creation.

Implementation Note: In a typical Guidewire implementation, this logic is often handled via 'Event Fired' rules or specific 'Exit Points' in the workflow. The system waits for the confirmation that the Total Loss calculation service has successfully returned a result. Once that transaction is committed and the score is persisted on the Vehicle or Exposure entity, the subsequent rule to generate the History Event can trigger successfully.

Consequently, Option C is the only viable placement in the process flow. It ensures that the prerequisite action (calculation) is complete and the required data payload (the score) is available for the subsequent action (logging the history event).